Sheet Classification Unrealized Gain

Balance Sheet Classification Valuation

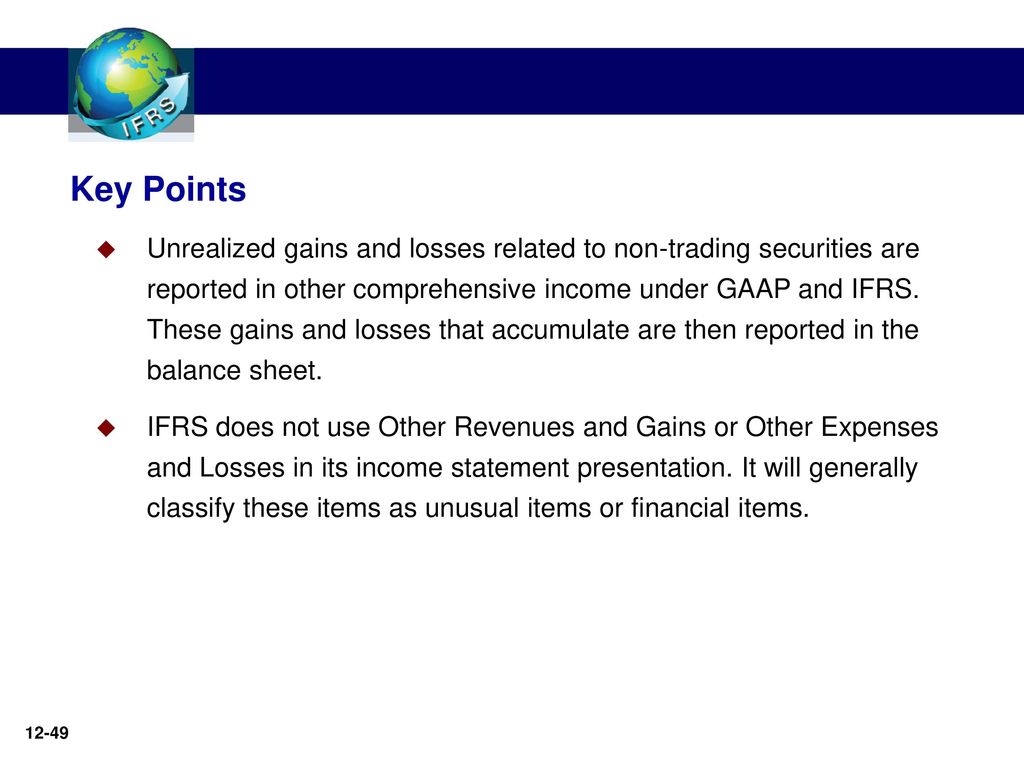

Other Comprehensive Income Overview Examples How It Works

Recording Unrealized Currency Gains And Losses Accountedge Knowledge Base

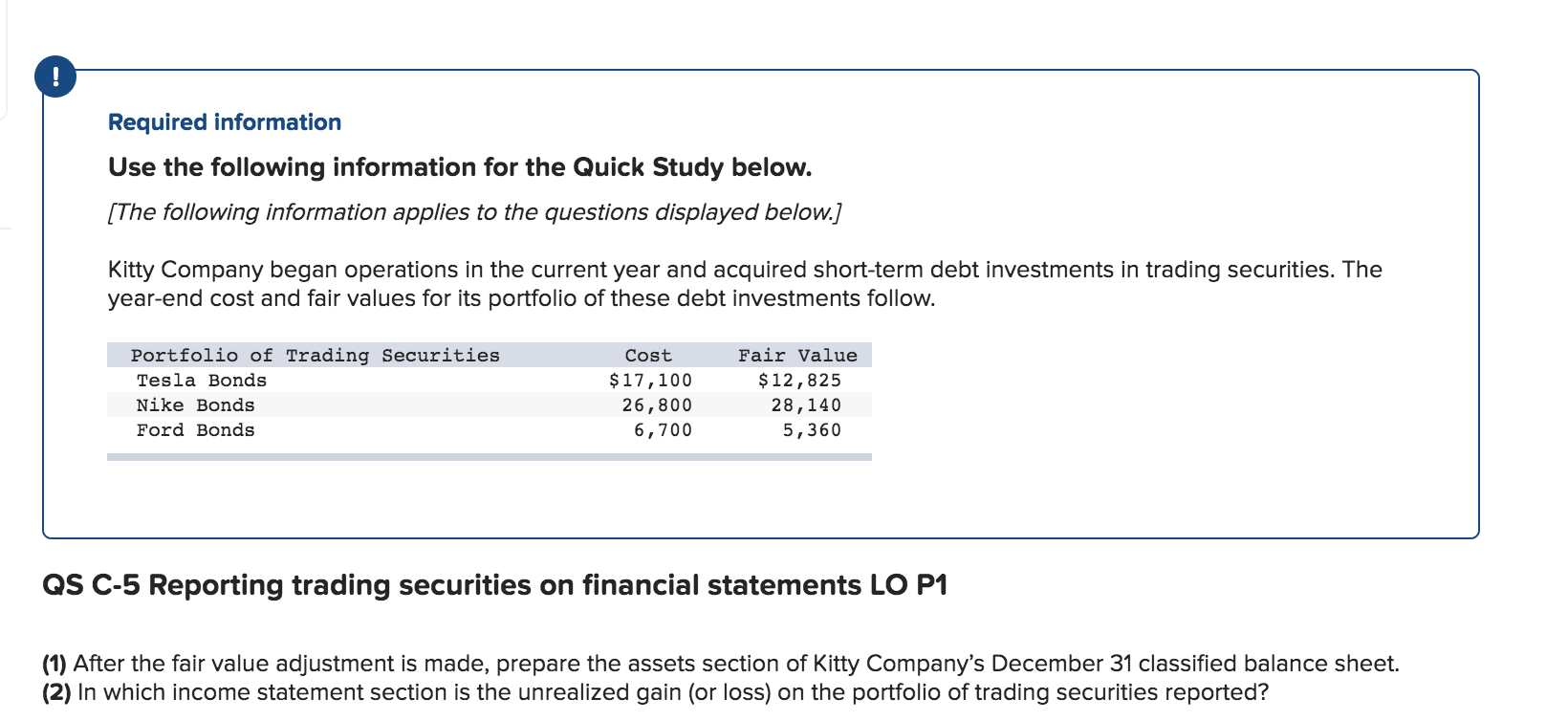

Required Information Use The Following Information Chegg Com

Available For Sale Securities Double Entry Bookkeeping

Debt Securities Principlesofaccounting Com

Increasing the asset available for sale securities and.

Sheet classification unrealized gain. An unrealized gain is the potential profit you could realize by cashing in the investment. Under the other assets section of the balance sheet. On paper the company made a paper profit of 5 000. However because you have not cashed in the investment the gain is currently unrealized.

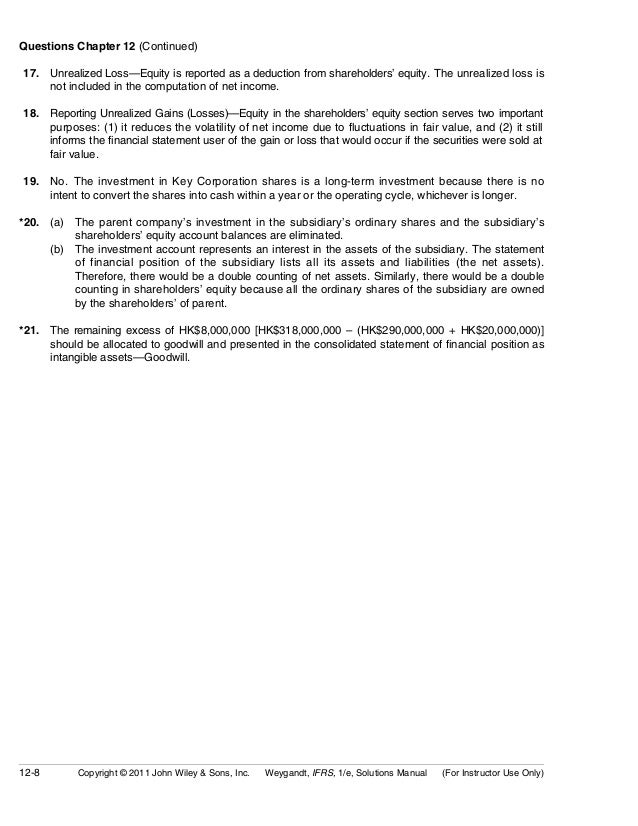

In the balance sheet the market value of short term available for sale securities is classified as short term investments also known as marketable securities and the unrealized gain loss account balance of 15 000 is considered a stockholders equity account and is part of comprehensive income. Each of these categories is treated differently and affects whether gains or losses appear on the balance sheet or income statement. If a company owns an asset and that asset increases in value then it may intuitively seem like the company earned a profit on that asset for example a company owns 10 000 worth of stock then the stock value rises to 15 000. The unrealized gain is however reported on the balance sheet by.

Such a gain is recorded in the balance sheet before the asset has been sold and thus the gains are called unrealized because no cash transaction happened. The entry to record the valuation adjustment is. Where do you post unrealized gains and losses on the balance sheet. Recording unrealized gains and losses is.

An unrealized gain is also referred to as a paper profit because the gain is only theoretical until you sell the investment. An unrealized gain is a profit that exists on paper resulting from an investment. Increasing the stockholders equity component accumulated other comprehensive income. The line item can be referred as unrealized gain loss on the stock portfolio.

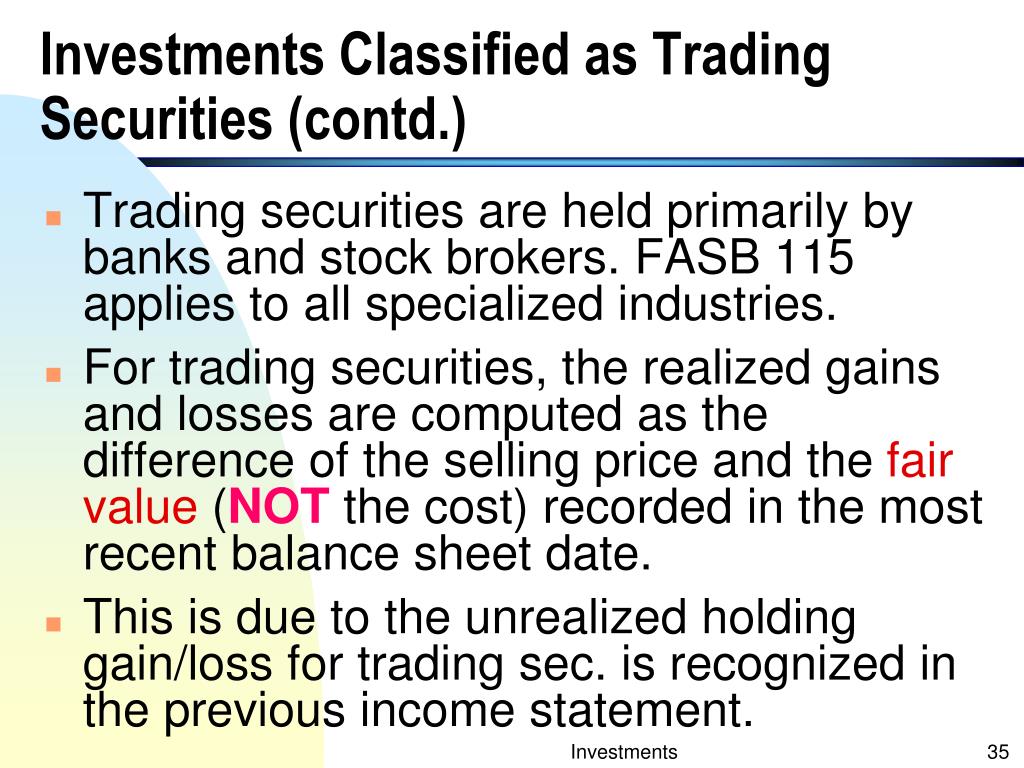

For securities except for trading securities the unrealized gains do not impact the net income. It is a profitable position that has yet to be sold in return for cash such as a stock position. The unrealized gains or losses are recorded in the balance sheet under the owner s equity owner s equity owner s equity is defined as the proportion of the total value of a company s assets that can be claimed by the owners sole proprietorship or partnership and by the shareholders if it is a corporation. Realized unrealized examples example 1.

Diagram Template Of Emergent Strategy Powerpoint Diagram Templates

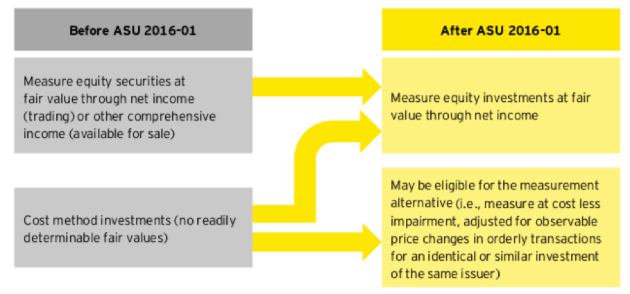

What Investors Need To Know About Asu 2016 01 S Impact On Invested Capital And Oci

Berkshire S Bottom Line More Relevant Than Ever Before Cfa Institute Market Integrity Insights

Examboat Kids Iq Test Exams Study Plan Test Exam Take Exam Exam

Top 15 Best Equity Mutual Funds For Sips Lump Sum Investments In 2016 Mutuals Funds Mutual Fund India Investing

Hs 440 Hs 440 Hs440 Unit 8 Assignment Kaplan

Chapetr 12 Investments Learning Objectives Ppt Download

What Are Unrealized Gains And Losses

Reading 14 Intercorporate Investments Flashcards Quizlet

Accounting Flashcards Quizlet

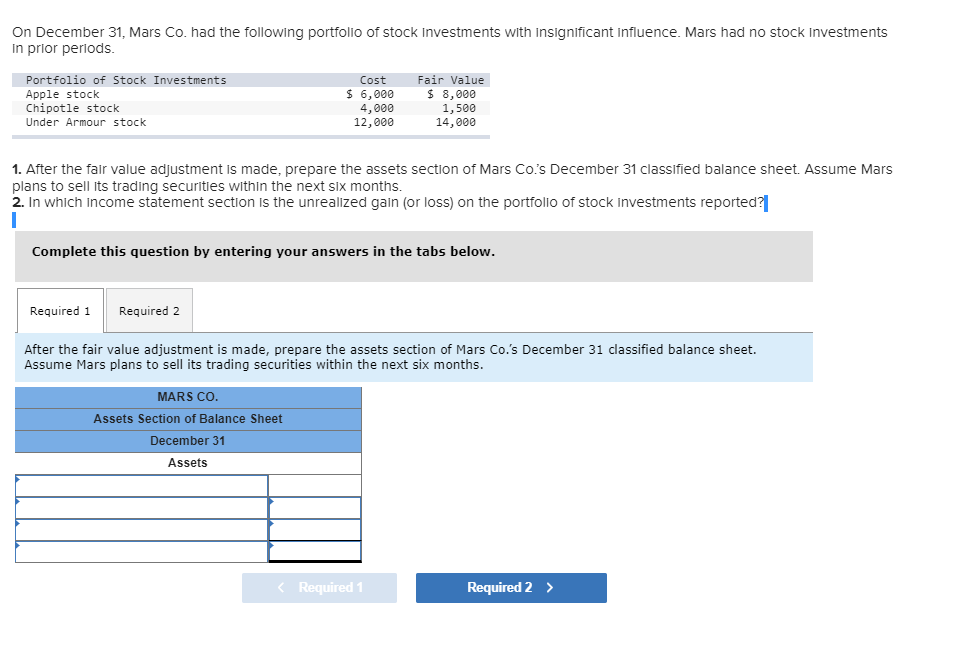

Solved On December 31 Mars Co Had The Following Portfol Chegg Com

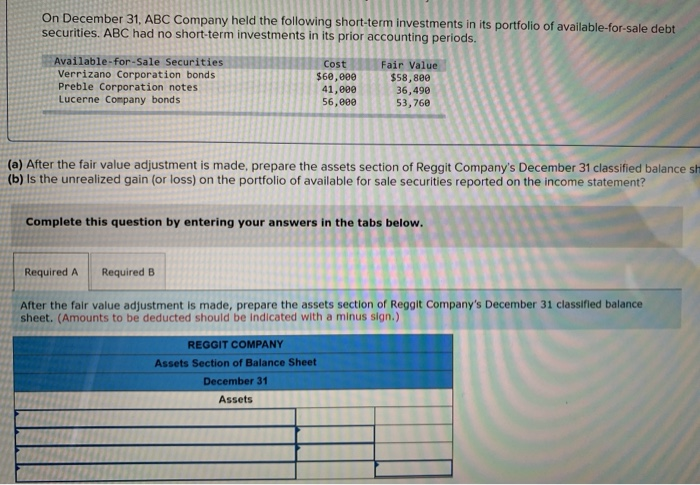

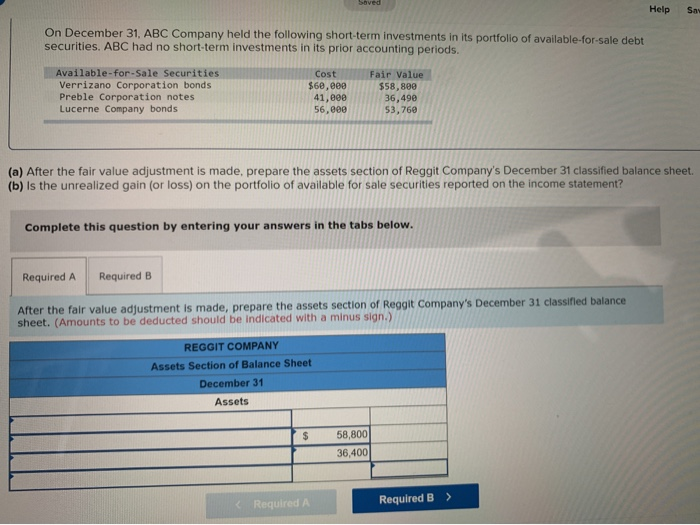

Solved On December 31 Abc Company Held The Following Sho Chegg Com

Balance Sheet Presentation Of Trading Investments During 2018 Its First Year Of Operations Galileo Company Purchased Homeworklib

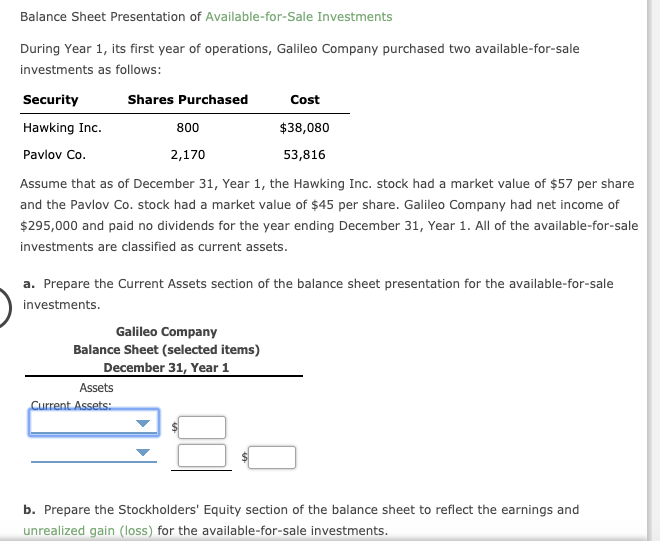

Solved Balance Sheet Presentation Of Available For Sale I Chegg Com

Solved Help Sa On December 31 Abc Company Held The Follo Chegg Com

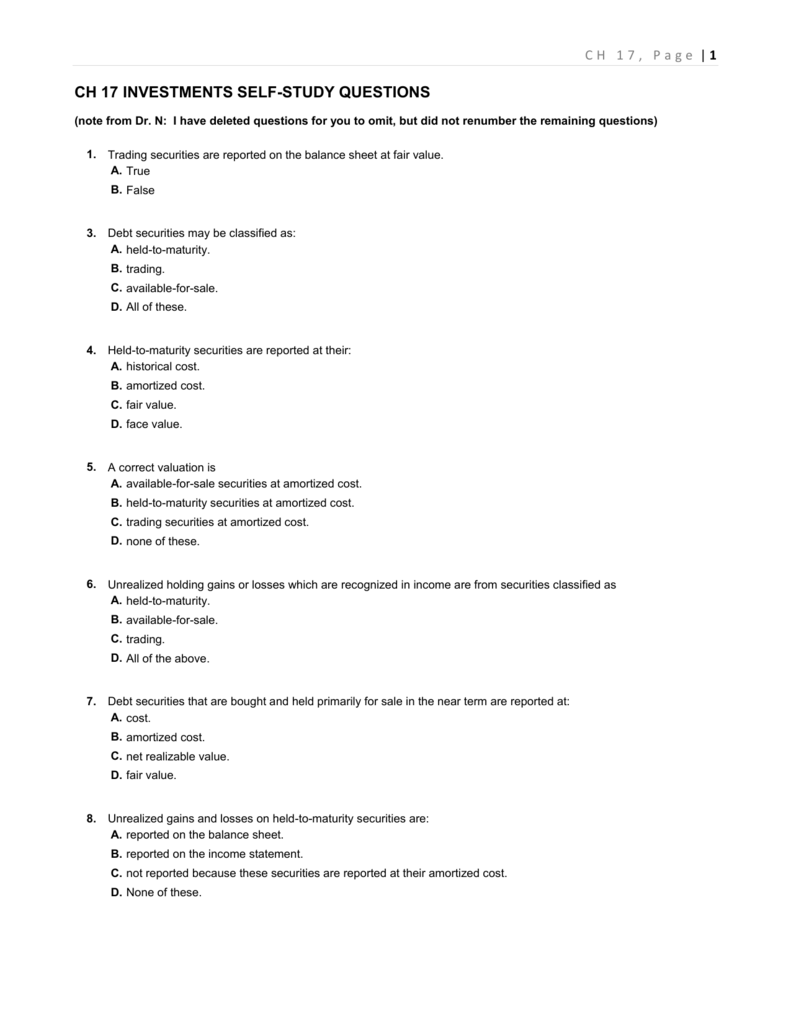

Ch 17 Investments Self

What Is An Unrealized Gain In An Income Statement Small Business Chron Com

:max_bytes(150000):strip_icc()/GettyImages-182178688-1e402e44fa754098b843dfa37331a1e2.jpg)

Unrealized Loss Definition

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gct0zmi0vurmwxhk9irpsv4tngmodtevf1qgpikflmleghyqlncz Usqp Cau

Management Decisions And Financial Accounting Reports Ppt Download

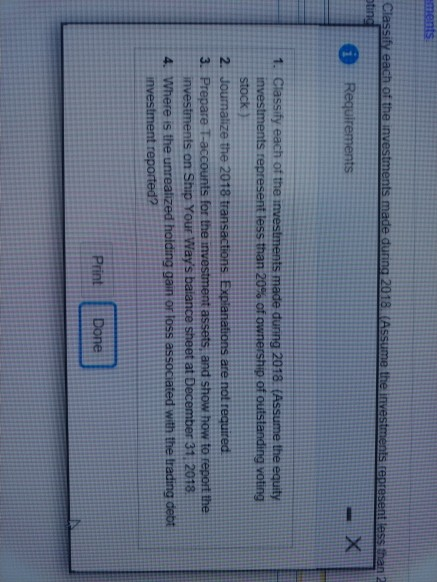

Solved Requirement 1 Classify Each Of The Investments Ma Chegg Com

Https Nanopdf Com Download Equity Method Investments Pdf

Management Decisions And Financial Accounting Reports Ppt Download

Https Papers Ssrn Com Sol3 Delivery Cfm Uva C 2240 Pdf Abstractid 1276984 Mirid 1

Solved Required Information The Following Information Ap Chegg Com

Wild 6th Ed Financial Managerial Appendix C

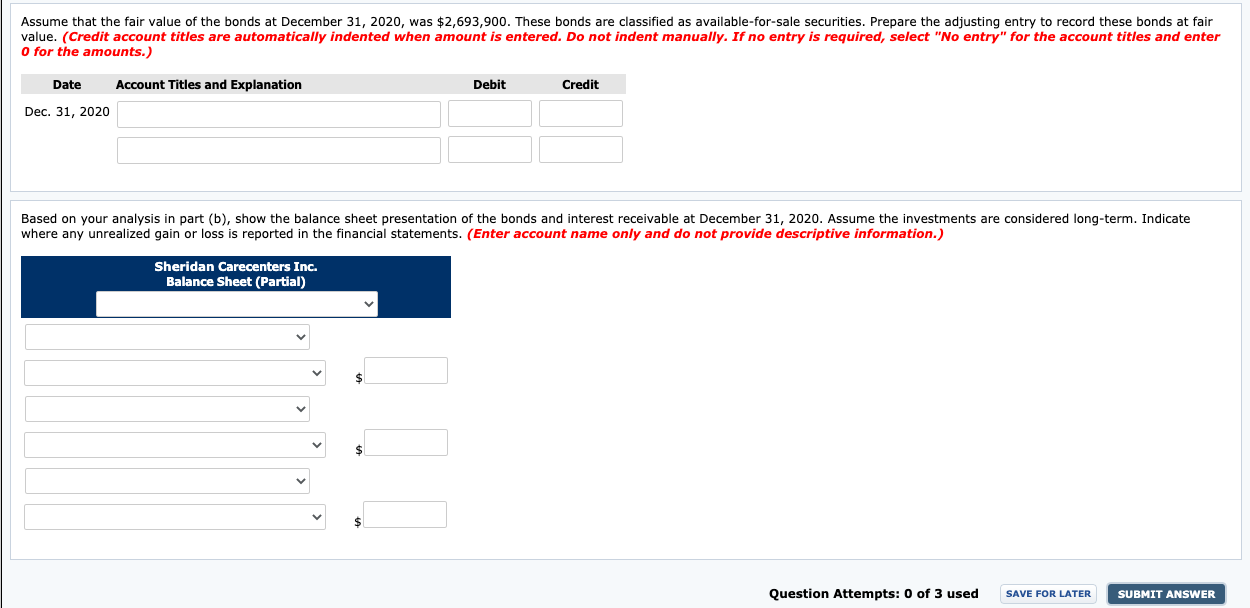

Problem 16 01a A C Video Sheridan Carecenters In Chegg Com

Ch17 Kieso Intermediate Accounting Solution Manual

Which Transactions Affect Retained Earnings

What Investors Need To Know About Asu 2016 01 S Impact On Invested Capital And Oci Seeking Alpha

Https Canvas Harvard Edu Files 5118266 Download Download Frd 1

Https Echalk Slate Prod S3 Amazonaws Com Private Classes 5290 Resources 711f064a 1003 4f2a 9b61 9e534d48431a Awsaccesskeyid Akiajszkibpxgflsztyq Expires 1812650388 Response Cache Control Private 2c 20max Age 3d31536000 Response Content Disposition 3bfilename 3d 22ch 252016 2520textbook Pdf 22 Response Content Type Application 2fpdf Signature Sd9rhdcplsj5zegrwbh2yyta5fm 3d

Ias 21 The Effects Of Changes In Foreign Exchange Rates Ifrsbox Making Ifrs Easy

Chapter 13 Managing The Investment Portfolio Ppt Download

Net Investment Income Nii Definition

Itau Unibanco Holding S A 2019 Foreign Issuer Report 6 K

/GettyImages-1160370731-dc3828fe158945d2ba6ff4dd3092f240.jpg)

Accounting For Intercorporate Investments

Solved Question Classification Reasons Requirements Trans Chegg Com

Prospect Capital Corp 2020 Investment Prospectus 497

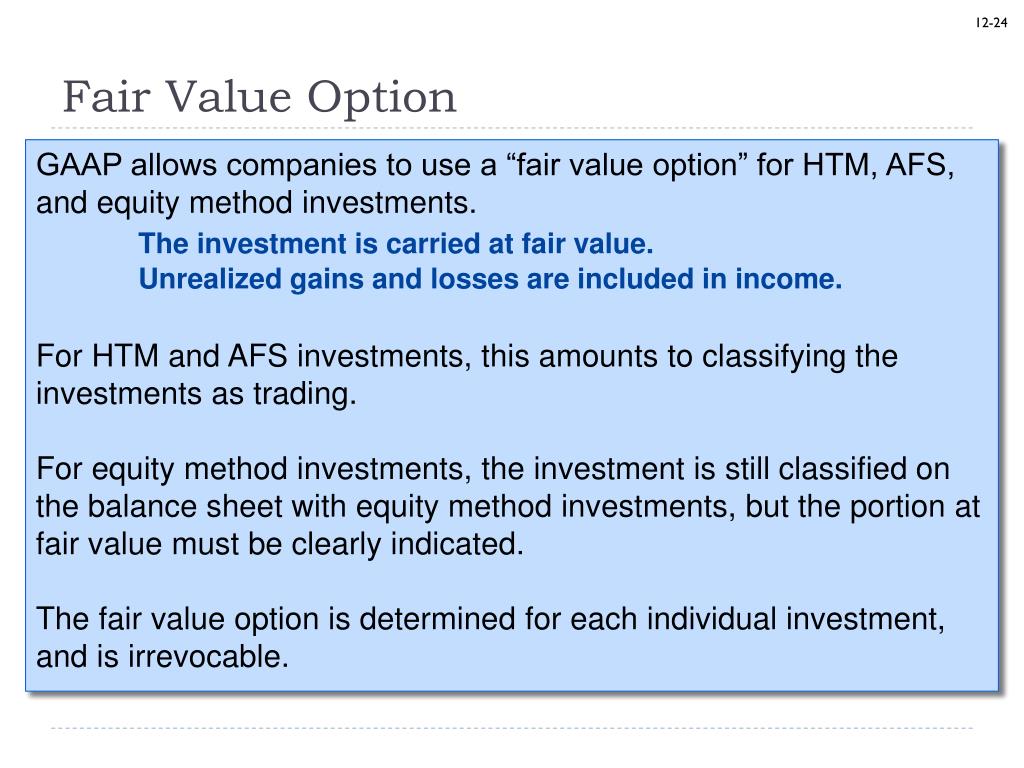

Investments Chapter 12 Learning Objectives Ppt Download

Ppt Chapter 12 Powerpoint Presentation Free Download Id 1039960

Ch12 Solution W Kieso Ifrs 1st Edi

Ppt Investments Powerpoint Presentation Free Download Id 3216612

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gctkulexulptxxtdpf7bcmutkke1ndxjiufzotssn6v93zctyydz Usqp Cau